Impairment Loss Journal Entry

The double entry to record an impairment loss is by debiting to the Impairment loss Account in PL in the period and then credited to the Accumulated Impairment losses Account in the Balance Sheet. Impairment loss under IFRS journal entriesdocx.

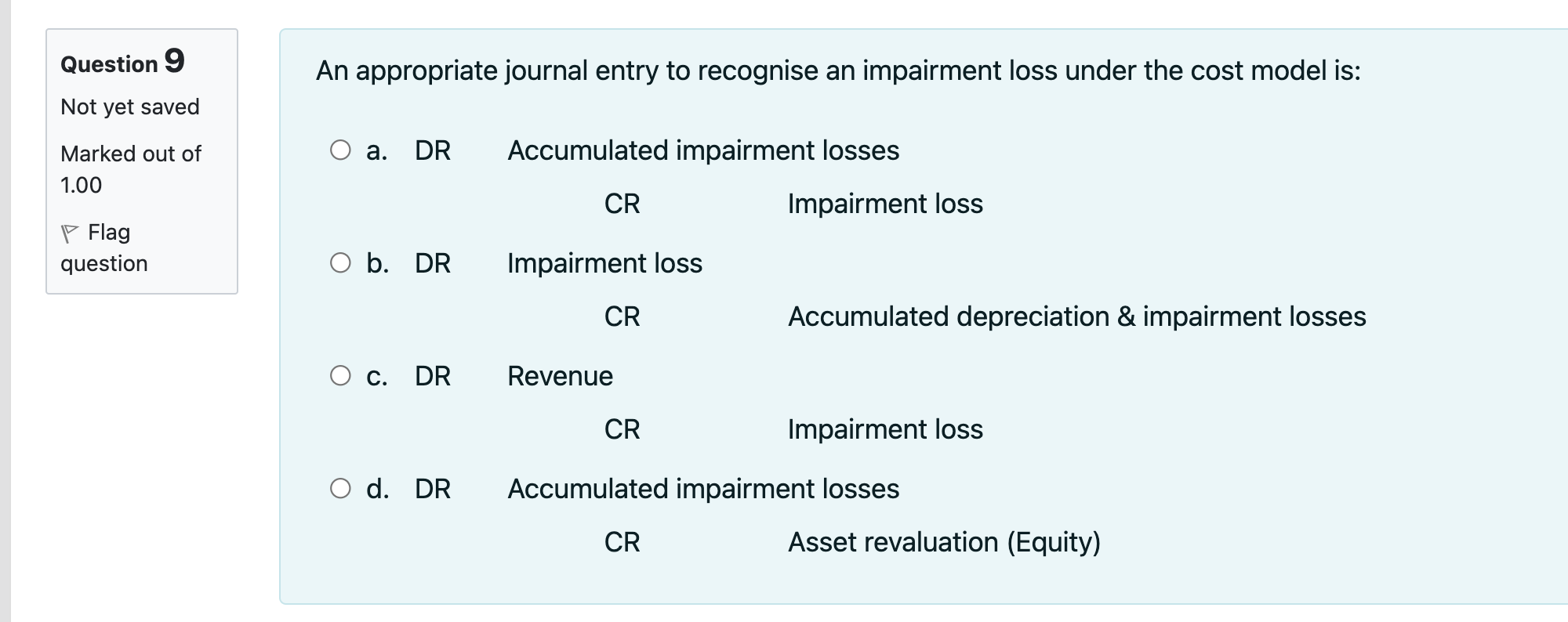

Solved Question 9 An Appropriate Journal Entry To Recognise Chegg Com

In this case the company ABC needs to make the fixed asset impairment journal entry for the impairment loss of 50000 due to obsolescence of its machine as below.

. Calicut University Study Centre in Ras Al Khaimah. The journal entry is debiting impairment expense 50 million and credit machinery 50 million. Kyle Taylor Founder at The Penny Hoarder 2010present Updated Jul 22 Youve done it.

Based on the report from a technical expert the impairment loss is 50 million. The company can make the journal entry for goodwill impairment by debiting the goodwill impairment account and crediting the goodwill account when it finds out that there is an impairment of goodwill as a result of periodic review. Thus the total impairment loss amounts to 1250000 2600000 1350000.

To increase to augment. Impairment loss under IFRS journal entriesdocx. Best answer Impairment loss is recognized immediately in PL unless the asset is carried at revalued amount Thus entries would be.

You can do this through a debit. Goodwill impairment is an expense item on the income statement in which its normal balance is on the debit side. According to IAS 36 goodwill should be tested for impairment at least annually.

Journal Entry to Recognize the ImpairmentLoss Impairment Loss Goodwill Accumulated Depreciation Patent -The carrying amount of an asset shall not be reduced below the highest fair value less cost of disposal value in use and zero -The amount of impairment loss that would otherwise have been allocated to the asset shall be allocated prorate to. The adjusted land value to be shown in the balance sheet under Fixed Assets is 300000. Likewise in this journal entry total assets on the balance sheet decrease by 20000 and total.

Company ABC Limited has identified an impairment loss of 300000 on one of its land which will not be recovered shortly soon. The impairment loss becomes a part of the Income Statement and reduces the profits of the company during the period. Dr Impairment losses ac PL account Cr Asset account ac Balance sheet account If the asset is carried at revalued amount impairment loss is treated as a reduction in revaluation gain.

Accounting Treatment for Impairment Impairment majorly constitutes a reduction in the value of an underlying asset. Asset is carried at cost model. The land cost 400000 two years ago.

Asset is carried at revaluation model and there is a balance of revaluation surplus of USD 300000 as at 31 December 2020. This loss generates from various sources. Calicut University Study Centre in Ras Al Khaimah FINANCE 15113.

Provide the journal entry for the impairment of loss. To provision for impairment loss account Promoted by The Penny Hoarder Should you leave more than 1000 in a checking account. Conclusion Impairment loss represents the difference between an assets recoverable and carrying values.

You must record your impairment loss by creating a new journal entry. Generally Accepted Accounting Principles. Record journal entries for recognizing impairment loss in the following two scenarios.

It order to do this Entity A needs to calculate the recoverable amount of all three CGUs to see if they cover the value of goodwill. Numbers are as follows. In order to record the reduction in the value of the asset the loss needs to be charged to the Income Statement as an expense.

Its market value suddenly plunged to 500. Impairment loss Recoverable amount Carrying value Impairment loss 400000 500000 Impairment loss 100000 ABC Co. Record the loss by increasing your Expense account.

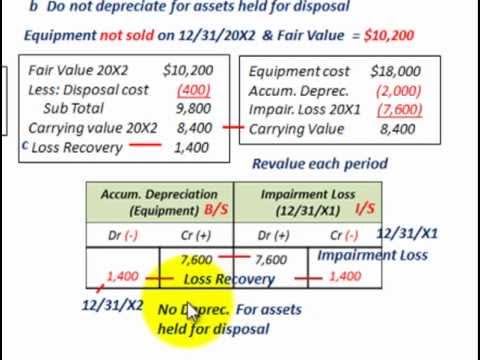

You need to follow AS 28 -impairment of fixed assets for this purpose and journal entry will be- Profit and loss account. To come to by way of increase. The decrease in the fair value in this case is 20000 160000 140000 and as the balance of revaluation surplus is only 18000 in above example the excess amount of 2000 20000 18000 will go to the impairment loss account.

The total carrying value for the CGU is 2600000 and the total estimated recoverable amount is 1350000. After dropping it down a flight of stairs it loses some functionality. You must record an impairment loss of 500.

Journal entry for impairment without revaluation surplus. So we need to reduce the balance of fixed assets machinery by 50 million and record impairment expenses. To arise or spring as a growth or result.

The journal entry above shows the write-off of an asset from the Balance Sheet. This impairment loss needs to be written off so that the assets value is not overstated on the balance sheet of Hightech Express. Write back accumulated depreciation 2.

Recognise the impairment loss where the decrement is less than the previous increments. Then records the impairment loss journal entry as follows. In this journal entry total expenses on the income statement increase by 50000 while total assets on the balance sheet decrease by 50000.

An impairment loss is recognized through a journal entry that debits Loss on Impairment debits the assets Accumulated Depreciation and credits the Asset to reflect its new lower value. When dealing with a depreciable asset where the impairment loss is more than the previous revaluation increase the journal entries are. Please record the journal entry of impairment loss.

As we can see CGU Z is impaired as its recoverable amount is lower by 2m than the carrying amount.

Accounting For Property Plant And Equipment Reversal Of Impairment Loss Part 1 Youtube

Accounting For Impairments Of Ppe Youtube

Impairment Loss Accounting Impairment Of Assets Held For Use Vs Intended For Disposal Youtube

Impairment Loss Accounting Impairment Of Assets Held For Use Vs Intended For Disposal Youtube

No comments for "Impairment Loss Journal Entry"

Post a Comment